Last Updated: 2026.04.09

to Chinese page

to Japanese page

Below is the summary announced on April 9 of Results Summary for FY2026 First Half (Six Months to February 2026).

Fiscal 2026 First-half Performance Highlights

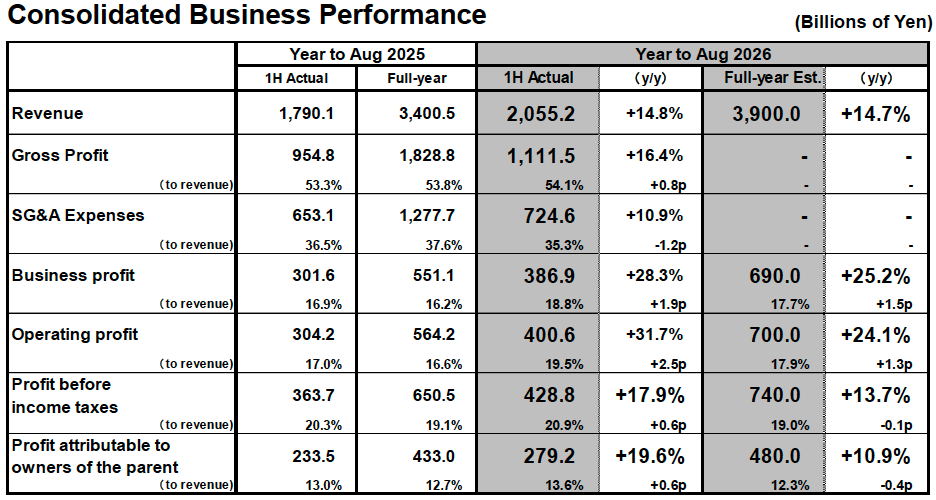

■Consolidated results: Fast Retailing reports a record performance on significant revenue and profit gains

- In the first half of FY2026, consolidated revenue rose to 2.0552 trillion yen (+14.8% year on year), business profit increased to 386.9 billion yen (+28.3%), and profit attributable to owners of the Parent expanded to 279.2 billion yen (+19.6%).

- UNIQLO operations reported revenue and profit gains across all regions thanks to our successful branding strategy, which is centered around the opening of flagship stores, and our strategic business approach to year-round products.

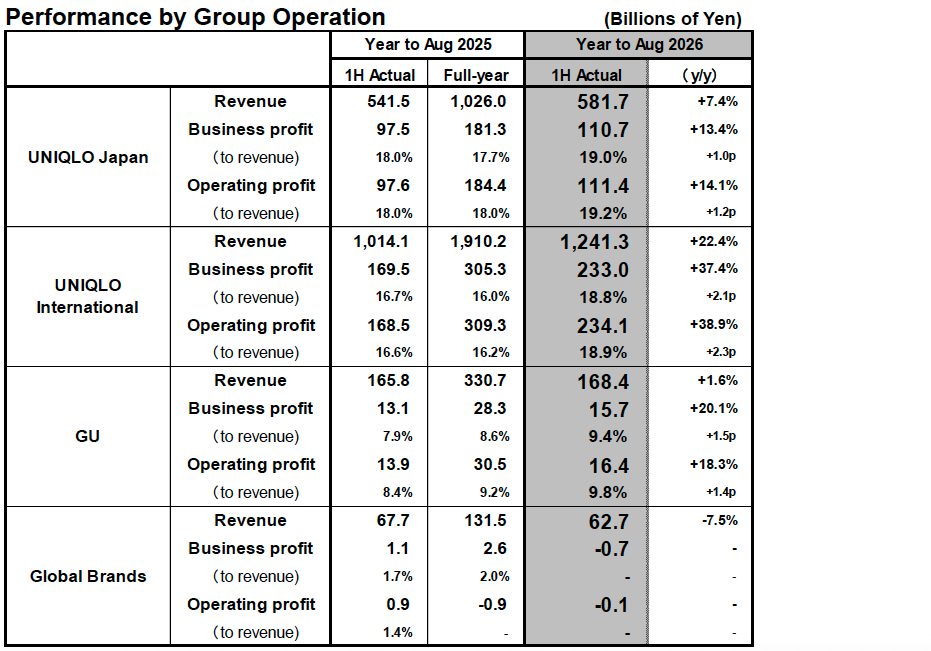

■UNIQLO Japan: Reports a rise in revenue and a sharp profit gain

- Revenue: 581.7 billion yen (+7.4%), business profit: 110.7 billion yen (+13.4%).

- Same-store sales expanded 6.5% thanks to strong sales of year-round products and buoyant sales of Winter ranges when the weather turned colder.

- The gross profit margin contracted by 0.2p due to a rise in cost of sales caused by a weakening in yen forward contract rates. The SG&A ratio improved by 1.2p due to lower personnel and store rent cost ratios.

■UNIQLO International: Considerable increases in both revenue and profit

- Revenue: 1.2413 trillion yen (+22.4%), business profit: 233.0 billion yen (+37.4%). Business profit margin improved by 2.1 points.

- UNIQLO's global presence is growing with the opening of more flagship and large-format stores worldwide.

- All markets reported strong sales performances, due not only to strong sales of Winter ranges, but also to efforts to enhance the appeal of year-round products.

- The Greater China region reported an increase in revenue and double-digit growth in profits. UNIQLO operations in South Korea, the Southeast Asia, Australia & India region, North America, and Europe continue to grow at a high rate, reporting double-digit revenue and profit growth in the first half.

■GU: Slight increase in revenue, significant increase in profit

- Revenue: 168.4 billion yen (+1.6%), business profit: 15.7 billion yen (+20.1%).

- This result was due to the strong sales of items that captured the latest mass fashion trends, and the strong performances of new GU stores in the Taiwan and Hong Kong markets.

- Improvements in the gross profit margin and SG&A ratio helped boost the business profit margin. The benefits of structural reforms are beginning to show, following efforts to tighten the number of products on offer by focusing on strong-selling items, as well as efforts to improve volume planning accuracy.

■Global Brands: Revenue declines and operation reports a business loss

- Revenue: 62.7 billion yen (−7.5%), business loss: 0.7 billion yen.

- The Theory operation reported a decline in revenue and a slight loss under the business profit(loss) category. Sales from Theory in the USA contracted as a result of a sluggish wholesale business, with poor-performing department stores and the closure of e-commerce outlet stores in March 2025. The USA operation also slipped into the red after recording bad debts associated with a wholesale department store partner that filed for bankruptcy.

■FY2026 consolidated estimates: Consolidated estimates revised up

- FY2026 consolidated revenue: 3.9000 trillion yen (+14.7%), consolidated business profit: 690.0 billion yen (+25.2%), consolidated operating profit: 700.0 billion yen (+24.1%), and profit attributable to owners of the Parent: 480.0 billion yen (+10.9%).

- These estimates include upward revisions of 100.0 billion yen for revenue, 40.0 billion yen for business profit, 50.0 billion yen for operating profit, and 30.0 billion yen for profit attributable to owners of the Parent.

- We forecast an annual dividend in FY2026 of 640 yen per share, split equally between interim and year-end dividends of 320 yen each. That would represent an increase in the annual dividend of 140 yen compared to FY2025.

Fiscal 2026 First-half Performance in Focus

■UNIQLO Japan: Reports a rise in revenue and a sharp profit gain

UNIQLO Japan reported an increase in revenue and a large expansion in profit in the first half of fiscal 2026, with revenue expanding to 581.7 billion yen (+7.4%) and business profit rising to 110.7 billion yen (+13.4%). First-half same-store sales (including e-commerce sales) increased by 6.5% year on year after a strategically selected lineup of year-round items helped to drive overall sales, and the onset of colder weather also generated strong sales of Winter ranges. The gross profit margin contracted by 0.2 points year on year due to the rise in cost of sales caused by weaker yen forward contract exchange rates used for procurement purposes. Meanwhile, the selling, general and administrative expense ratio improved by 1.2 points year on year, with the strong sales performance resulting in lower personnel and store rent component ratios.

■UNIQLO International: Considerable increases in both revenue and profit

UNIQLO International reported significant increases in revenue and profit in the first half of fiscal 2026, with revenue rising to 1.2413 trillion yen (+22.4%) and business profit expanding to 233.0 billion yen (+37.4%).

Breaking down the UNIQLO International performance into individual regions and markets, among UNIQLO operations in the Greater China region, the Mainland China market reported a rise in first-half revenue and double-digit year-on-year growth in first-half profit. Strong sales were recorded in the second quarter from December 2025 to February 2026 following efforts to respond to warmer weather by proactively presenting styling options for bottoms, sweatshirts/pants, casual outerwear, and other Spring and year-round items during the Chinese New Year sales period. The Hong Kong market reported a rise in first-half revenue but a decline in profit. However, profit increased year on year when royalty fees were excluded. The Taiwan market reported higher revenue and profit.

Meanwhile, UNIQLO South Korea achieved double-digit growth in both revenue and profit thanks to the successful use of digital channels to communicate strategic product information and a continued rise in support for UNIQLO primarily among younger customers. UNIQLO operations in Southeast Asia, India & Australia reported double-digit revenue and profit growth for the first half. Our decision to strategically expand Winter inventory and sales floor displays contributed to the strong sales performance. Buoyant sales of bottoms, short-sleeved knitwear, linen shirts, and other Spring Summer ranges also helped drive higher revenue and profit figures across all operations in the region.

UNIQLO North America and UNIQLO Europe continued to generate high levels of growth, reporting double-digit rises in first-half revenue and profit. The two operations recorded double-digit growth in same-store sales after HEATTECH, down, and other Winter ranges sold well and sweatshirts/pants, bottoms, and other year-round items also helped drive sales.

■GU: Slight increase in revenue, significant increase in profit

GU reported a slight rise in revenue and a double-digit expansion in profit in the first half of fiscal 2026, with revenue increasing to 168.4 billion yen (+1.6%) and business profit expanding to 15.7 billion yen (+20.1%). Revenue was supported by strong global sales of soft sheer crew neck T-shirts, gathered ballet sneakers, and other items that captured mass fashion trends and boosted brand popularity among young customers, as well as the strong sales performance of new GU stores in Taiwan and Hong Kong. The business profit margin improved on the back of improvements in the gross profit margin and the selling, general and administrative expense ratio. Those improvements were the result of ongoing operational reforms, such as the narrowing of GU product offerings and concentration on strong-selling items, as well as more accurate volume planning.

■Global Brands: Revenue declines and operation reports a business loss

In the first half of fiscal 2026, Global Brands reported a decline in revenue to 62.7 billion yen (−7.5%) and a loss of 0.7 billion yen under the business profit/loss category (compared to a 1.1 billion yen profit in the first half of fiscal 2025). This was due primarily to sluggish Theory brand sales. The overall Theory business recorded a decline in revenue and a slight business loss, mainly due to lower revenue and a business loss in Theory USA. Theory USA revenue contracted as a result of a sluggish wholesale business, with poor-performing department stores and the closure of e-commerce outlet stores in the USA in March 2025. On the profit front, the overall loss at Theory was caused primarily by the recording of bad debts after a wholesale department store partner filed for bankruptcy. Regarding other labels in the Global Brands segment, PLST reported higher revenue and double-digit profit growth in the first half thanks to strong sales of menswear items such as rayon blend shirts and Precious Knit Melton items, along with a sharp rise in e-commerce sales. Finally, our combined Comptoir des Cotonniers and Princesse tam.tam business reported a decline in revenue, resulting from a roughly 50% reduction in the number of stores at end-February compared to the previous year, as part of overall restructuring efforts and our drive to create a concentrated urban network. The reduction in unprofitable stores and reformed cost structures did, however, help improve the selling, general and administrative expense ratio and reduce overall losses.

■FY2026 consolidated estimates: Consolidated estimates revised up

In fiscal 2026, the Fast Retailing Group expects to achieve a record performance by reporting consolidated revenue of 3.9000 trillion yen (+14.7%), business profit of 690.0 billion yen (+25.2%), operating profit of 700.0 billion yen (+24.1%), and profit attributable to owners of the Parent of 480.0 billion yen (+10.9%). Compared to the performance estimates announced in January 2026, the new forecasts include an upward revision of 100.0 billion yen for revenue, 40.0 billion yen for business profit, 50.0 billion yen for operating profit, and 30.0 billion yen for profit attributable to owners of the Parent. These upward revisions reflect: (1) the stronger-than-anticipated first-half performance; (2) an upward revision in second-half estimates in view of the current sales environment; and (3) revised second-half exchange rate assumptions to incorporate recent yen weakness. We have also increased our expected annual dividend per share for fiscal 2026 by 100 yen, to 640 yen, which comprises interim and year-end dividends of 320 yen each. That would represent an increase in the full-year dividend of 140 yen per share compared to the previous year.

Regarding our forecasts for each of our four business segments, we expect UNIQLO International will generate double-digit revenue and profit growth in the second half of fiscal 2026 and the full fiscal year. Within that segment, markets in the Greater China region are expected to report year-on-year increases in revenue and profit in the second half of the year, and an increase in revenue and double-digit profit growth in fiscal 2026. UNIQLO operations in South Korea, the Southeast Asia, India & Australia region, North America, and Europe are all expected to continue expanding, and generate double-digit revenue and profit growth in the second half and the full business year.

At UNIQLO Japan, second-half revenue is expected to rise, and second-half business profit is forecast to hold steady at the previous year's level. While the second-half SG&A ratio is expected to improve slightly as productivity gains help reduce the personnel cost and other component ratios, the gross profit margin is forecast to deteriorate slightly as a depreciation in the yen results in higher cost of sales. Full-year estimates for UNIQLO Japan predict year-on-year growth in both revenue and profit. Meanwhile, GU is expected to report higher revenue and double-digit profit growth in the second half and for the fiscal year as a whole. Finally, the Global Brands segment is expected to generate higher revenue and profit in the second half, and a slight decline in revenue but an increase in business profit for fiscal 2026 as a whole.

Estimates incorporate some impact from the Middle East situation, based on current considerations such as higher transportation costs in some markets. For the 2026 fiscal year, we have already progressed production and taken measures on transportation, so no major impact is expected from a production and logistics perspective. If there is any significant change to the currently-assumed business environment, we will review our earnings forecasts as appropriate.

Fast Retailing Co., Ltd. discloses business results data and offers a variety of press releases on its IR website https://www.fastretailing.com/eng/ir/.

Fast Retailing Co., Ltd. discloses business results data and offers a variety of press releases on its IR website https://www.fastretailing.com/eng/ir/.